box-pierce distribution The Box–Pierce test uses the test statistic, in the notation outlined above, given byand it uses the same . See more With wood modular construction, I like to say the best strategy is to design for the minimum number of maximum sized boxes, which also get the most bang for the buck on the shipping expenses. Steel modular is a bit .

0 · box.test: Box

1 · R: Box

2 · Ljung–Box test

3 · Ljung Box Test: Definition

4 · LECTURE ON TIME SERIES DIAGNOSTIC TESTS

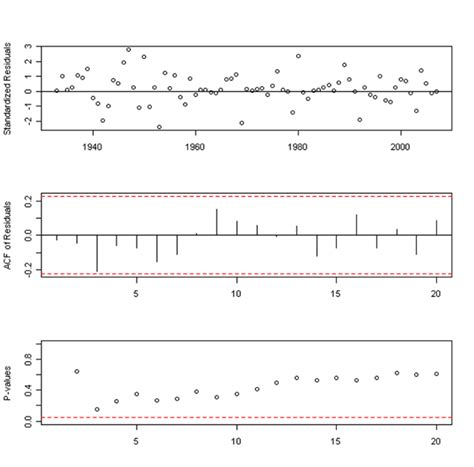

5 · How many lags to use in the Ljung

6 · Box–Pierce test

7 · Box

8 · Bootstrapping the Box–Pierce Q test: A robust test of

9 · 3.2 Diagnostics

Metal fabricators are skilled professionals who design, cut, weld, shape, and assemble metal components to create various structures or parts. They work with many .

The Ljung–Box test (named for Greta M. Ljung and George E. P. Box) is a type of statistical test of whether any of a group of autocorrelations of a time series are different from zero. Instead of testing randomness at each distinct lag, it tests the "overall" randomness based on a number of lags, and is . See moreThe Ljung–Box test may be defined as:$${\displaystyle H_{0}}$$: The data are independently distributed (i.e. the correlations in the population from which the sample is taken are 0, so that any observed . See more

• Q-statistic• Wald–Wolfowitz runs test• Breusch–Godfrey test• Durbin–Watson test See more

• Brockwell, Peter; Davis, Richard (2002). Introduction to Time Series and Forecasting (2nd ed.). Springer. pp. 35–38. See moreThe Box–Pierce test uses the test statistic, in the notation outlined above, given byand it uses the same . See more

• R: the Box.test function in the stats package• Python: the acorr_ljungbox function in the statsmodels package• Julia: the Ljung–Box tests and the Box–Pierce tests in the HypothesisTests package See moreThis article incorporates public domain material from the National Institute of Standards and Technology See more

box.test: Box

The Ljung-Box statistic, also called the modified Box-Pierce statistic, is a function of the accumulated sample autocorrelations, r j, up to any specified time lag \(m\). As a function of .

The Ljung (pronounced Young) Box test (sometimes called the modified Box-Pierce, or just the Box test) is a way to test for the absence of serial autocorrelation, up to a specified lag k. The test is closely related to the Ljung & Box (1978) autocorrelation test, and it used to determine the existence of serial correlation in the time series analysis. The test works with chi-square distribution by the way.

The asymptotic distribution of the Box-Pierce and Ljung-BoxQ tests is derived under the assumption that {y t } is serially independent. This distribution result

Box-Pierce and Ljung-Box Tests Description. Compute the Box–Pierce or Ljung–Box test statistic for examining the null hypothesis of independence in a given time series. These are .

R: Box

The point exactly is that without strict exogeneity, the Box-Pierce/Ljung-Box do not have an asymptotic chi-square distribution, this is what the mathematics above show. Weak exogeneity (which holds in the above .

In this paper, a block bootstrap procedure is used to estimate the distribution of the QK statistic when the data are uncorrelated but dependent. The paper presents the results of a Monte . A test to determine whether a time series consists simply of random values (white noise). The test statistic is Qm, given by , where r is the sample autocorrelation at lag l, m is .

The Ljung–Box test (named for Greta M. Ljung and George E. P. Box) is a type of statistical test of whether any of a group of autocorrelations of a time series are different from zero.The Ljung-Box statistic, also called the modified Box-Pierce statistic, is a function of the accumulated sample autocorrelations, r j, up to any specified time lag \(m\). As a function of \(m\), it is determined as: \(Q(m) = n(n+2)\sum_{j=1}^{m}\frac{r^2_j}{n-j},\)

Compute the Box–Pierce or Ljung–Box test statistic for examining the null hypothesis of independence in a given time series. These are sometimes known as ‘portmanteau’ tests. a numeric vector or univariate time series. the statistic will be based on lag autocorrelation coefficients. test to be performed: partial matching is used.The Ljung (pronounced Young) Box test (sometimes called the modified Box-Pierce, or just the Box test) is a way to test for the absence of serial autocorrelation, up to a specified lag k.

The test is closely related to the Ljung & Box (1978) autocorrelation test, and it used to determine the existence of serial correlation in the time series analysis. The test works with chi-square distribution by the way.The asymptotic distribution of the Box-Pierce and Ljung-BoxQ tests is derived under the assumption that {y t } is serially independent. This distribution resultBox-Pierce and Ljung-Box Tests Description. Compute the Box–Pierce or Ljung–Box test statistic for examining the null hypothesis of independence in a given time series. These are sometimes known as ‘portmanteau’ tests. Usage Box.test(x, lag = 1, type = c("Box-Pierce", "Ljung-Box"), fitdf = 0) Arguments The point exactly is that without strict exogeneity, the Box-Pierce/Ljung-Box do not have an asymptotic chi-square distribution, this is what the mathematics above show. Weak exogeneity (which holds in the above model) is not enough for them.

Ljung–Box test

In this paper, a block bootstrap procedure is used to estimate the distribution of the QK statistic when the data are uncorrelated but dependent. The paper presents the results of a Monte Carlo investigation of the numerical performance of this bootstrap procedure. Under these conditions the Ljung-Box $Q$-statistic (which is a corrected-for-finite-samples variant of the original Box-Pierce $Q$-statistic), has asymptotically a chi-squared distribution, and its use has asymptotic justification.

The Ljung–Box test (named for Greta M. Ljung and George E. P. Box) is a type of statistical test of whether any of a group of autocorrelations of a time series are different from zero.The Ljung-Box statistic, also called the modified Box-Pierce statistic, is a function of the accumulated sample autocorrelations, r j, up to any specified time lag \(m\). As a function of \(m\), it is determined as: \(Q(m) = n(n+2)\sum_{j=1}^{m}\frac{r^2_j}{n-j},\)Compute the Box–Pierce or Ljung–Box test statistic for examining the null hypothesis of independence in a given time series. These are sometimes known as ‘portmanteau’ tests. a numeric vector or univariate time series. the statistic will be based on lag autocorrelation coefficients. test to be performed: partial matching is used.The Ljung (pronounced Young) Box test (sometimes called the modified Box-Pierce, or just the Box test) is a way to test for the absence of serial autocorrelation, up to a specified lag k.

The test is closely related to the Ljung & Box (1978) autocorrelation test, and it used to determine the existence of serial correlation in the time series analysis. The test works with chi-square distribution by the way.The asymptotic distribution of the Box-Pierce and Ljung-BoxQ tests is derived under the assumption that {y t } is serially independent. This distribution resultBox-Pierce and Ljung-Box Tests Description. Compute the Box–Pierce or Ljung–Box test statistic for examining the null hypothesis of independence in a given time series. These are sometimes known as ‘portmanteau’ tests. Usage Box.test(x, lag = 1, type = c("Box-Pierce", "Ljung-Box"), fitdf = 0) Arguments The point exactly is that without strict exogeneity, the Box-Pierce/Ljung-Box do not have an asymptotic chi-square distribution, this is what the mathematics above show. Weak exogeneity (which holds in the above model) is not enough for them.

junction box smzpcjb1uc

In this paper, a block bootstrap procedure is used to estimate the distribution of the QK statistic when the data are uncorrelated but dependent. The paper presents the results of a Monte Carlo investigation of the numerical performance of this bootstrap procedure.

junction box terminal block

Black asphalt shingles are classic, but consider your region. Matching new roof shingles to your house’s color scheme is an important decision. The color of a roof can completely change the look of a home, and replacing the roof can greatly improve your home’s curb appeal.

box-pierce distribution|How many lags to use in the Ljung